An issue of concern recently raised is; there is a lot of movement between the scheme providers which is not very productive, some KiwiSaver members are transferring between the scheme providers three or four times a year, we can’t understand why.

Continue readingTypes of Investments

The types of investments you should consider will depend on your investment profile which takes into account your personal circumstances and financial situation. It will also depend on your goals.

Continue readingAML & CFT – What’s it all about?

Operating as a financial advisory firm with an Authorised Financial Adviser meeting face to face with investing clients it is incumbent on me to ensure that we meet the requirements of the Anti Money Laundering and Counter Financing of Terrorism Act 2009 by providing suitable client identification prior to carrying out transactions.

Continue readingMighty River Power Share offer

FAQs for potential retail investors

Continue readingGoals and Risk Tolerance

Get to know yourself. Everybody is different.

To choose the right investment strategy, you need to be clear about your own needs and what you are trying to achieve.

INVESTMENT REVIEW – Presentation by NZ Funds

On Monday 8th April three members of the NZ Funds Management Ltd (NZF) team travelled up from Auckland and provided a yummy lunch and a one hour presentation on:

- Behavioural Finance

- Investment Review 2013

- Helping NZers become savers

Behavioural Finance: It was interesting to see the figures showing that the average returns over the past 25 years for Term Deposits 5.2%; Govt Bonds 5.2%; NZ Shares 5.7%; Global Shares 6.7%; NZ House prices 6.5% were within a very narrow band over that length of time.Inflation over that same 25 years averaged 2.6%.

With all of the market volatility experienced over the past decade it is understandable (and interesting) that according to Statistics NZ the average NZ house was held for 17 years yet shares were being held on average for a much shorter period of time……in the US it was just 6 months in 2010 according to Business Insider.

As pointed out above, Global Shares provided a return of 6.7% and NZ House prices 6.5% over the past 25 years so why hold onto houses and sell shares?

Why don’t we go the distance?

As advisers we assess your risk tolerance on a regular basis but what about your emotional composure? Are you always composed? Are you up and down? Are you always anxious?

Applying an accurate tolerance to risk is important, and STEP ONE.

STEP TWO is to ensure that you are appropriately diversified. The figures above support our stance on this matter.

STEP THREE is about averaging in and out of a portfolio rather than taking lump sums and similarly, placing large sums all on the one day.

Investment Review 2013: Not all inflation is created equal.

If you think about it the cost of communications has reduced since about the year 2000, and the cost of a new shirt or pair of shoes is probably about the same as it was back then, and the cost of recreation has risen only very slightly.

On the other hand we all know too well how the cost of housing and the power bill and water bill has risen over that same period of time, along with the cost of healthcare and what we call consumer staples such as food.

The investment managers at NZF continue to analyse and research ways of mitigating the effects of inflation on your portfolio by having an appropriate exposure to shares and bonds in companies which are most likely to provide this protection of the purchasing power of your retirement capital throughout your retirement years.

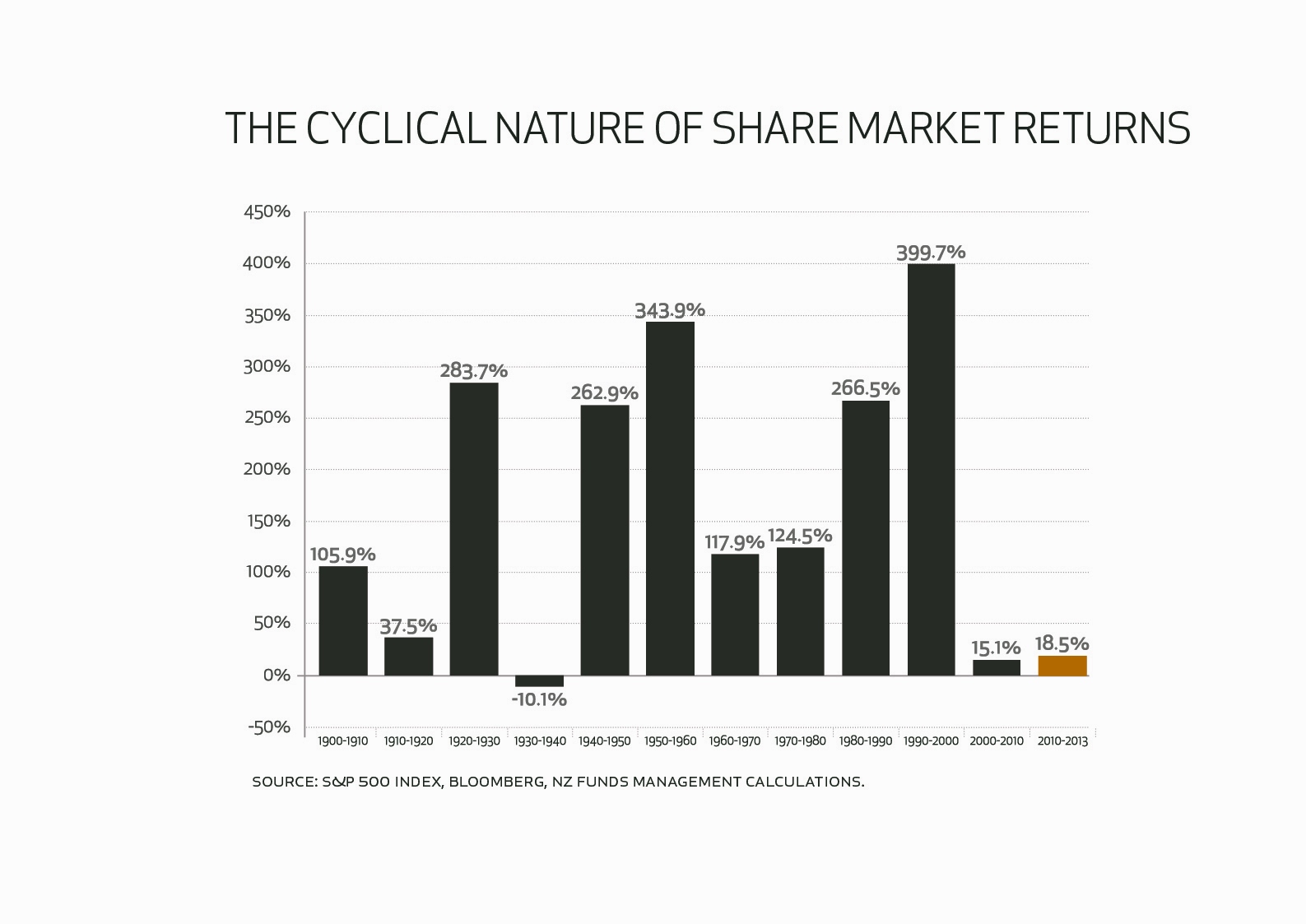

It is also very important to be aware of the cyclical nature of share market returns over time.

The graph illustrates the accumulated effect of 10 decades from 1900 to 2010. As you can see, the first 3 years of the current decade has already provided more of a positive result than the previous 10 years, 2000 – 2010, and as can also be seen, previous poor decades have been followed by strong results. No one is projecting anything here, it’s simply interesting to observe the trends over 100 years.

The graph illustrates the accumulated effect of 10 decades from 1900 to 2010. As you can see, the first 3 years of the current decade has already provided more of a positive result than the previous 10 years, 2000 – 2010, and as can also be seen, previous poor decades have been followed by strong results. No one is projecting anything here, it’s simply interesting to observe the trends over 100 years.

Helping NZers become savers: New Zealand’s population mix is changing. In 1976, just 8.8% of the population was over 65 years old. In 2006 this figure had risen to 12%. Statistics NZ estimate that by 2061 this figure will have reached 27%. Obviously the question is “can this country afford to continue to provide universal super at the current rate?”

Calculations and assumptions have been made by NZF showing that in 2013 NZers are saving 6%, and figures in 2012 put Australia 9%, UK 9.7%, USA 10% and Singapore a whopping 35.5%.

KiwiSaver funds total approximately $12b at present and are estimated to reach $100b by 2027 however this is unlikely to be sufficient to meet retirement funding requirements for most Kiwis.

Smart Solutions for Savers are available to you now. If you or someone you know may benefit from having us email you our Financial planning software myWealth we would be pleased to assist. You can either email or telephone your request to us.

Alternatively we would be delighted to take you through the software here in one of our offices especially set up for this purpose with a big screen. The coffee is great too, just like going to the movies. We look forward to hearing from you.

In conclusion, we have available a small supply of a booklet covering the presentation. If you would like one please let us know.

If you would like to revisit your own tolerance to risk and/or meet with me to discuss further any of the contents of this topic or anything else investment related, including a test drive of our myWealth software we would be delighted to hear from you.

Bill’s in the spotlight

WOW – We are extremely proud. Bill has been published in the latest issue of ASSET magazine.

Here he is hot of the press!

ASSET – Bill Raynel is a man on a misson

ASSET Magazine was launched in 2002 and is a distinctive, high quality publication that delivers in-depth analysis of the key concerns for financial advisers such as regulation, tax changes and KiwiSaver. Taking the issues one step further, ASSET discusses the people, producs and passions of the financial services industry. A monthly publication targeted to all those who provide financial services advise, including financial planners, investment advisers, fund managers, brokers, risk advisers, lawyers and accountants.

Why SAVE for Retirement?

For some of us Retirement seems a long way off. Many of us will be relying on NZ Super and our own savings for income in retirement. But how much do we actually need? This will depend on your own circumstances. What we do know is the sooner you start the more you will have.

Continue readingFMA Update “KiwiSaver – Are you getting the right advice”

FMA has launched a new consumer brochure to help New Zealanders understand the different types of services they may receive when investing in KiwiSaver shcemes or considering changing between schemes or funds.

Understanding the service you receive is the key step to making informed decisions about your money.

Continue readingDefaulting on $72,000 in KiwiSaver

Classical investment advice is that long-term investors should invest in growth assets (eg: shares and property) and switch gradually to income assets (eg: cash and fixed interest) as they get older. Growth assets should do well over long periods of time but they are volatile. Income assets produce lower returns over time but they are more stable. This strategy should result in a reasonable return at a reasonable level of risk.

Continue reading